Municipal bonds often reward investors who read and research patiently before acting. They can also punish those who stop at the rating, coupon, yield, and maturity.

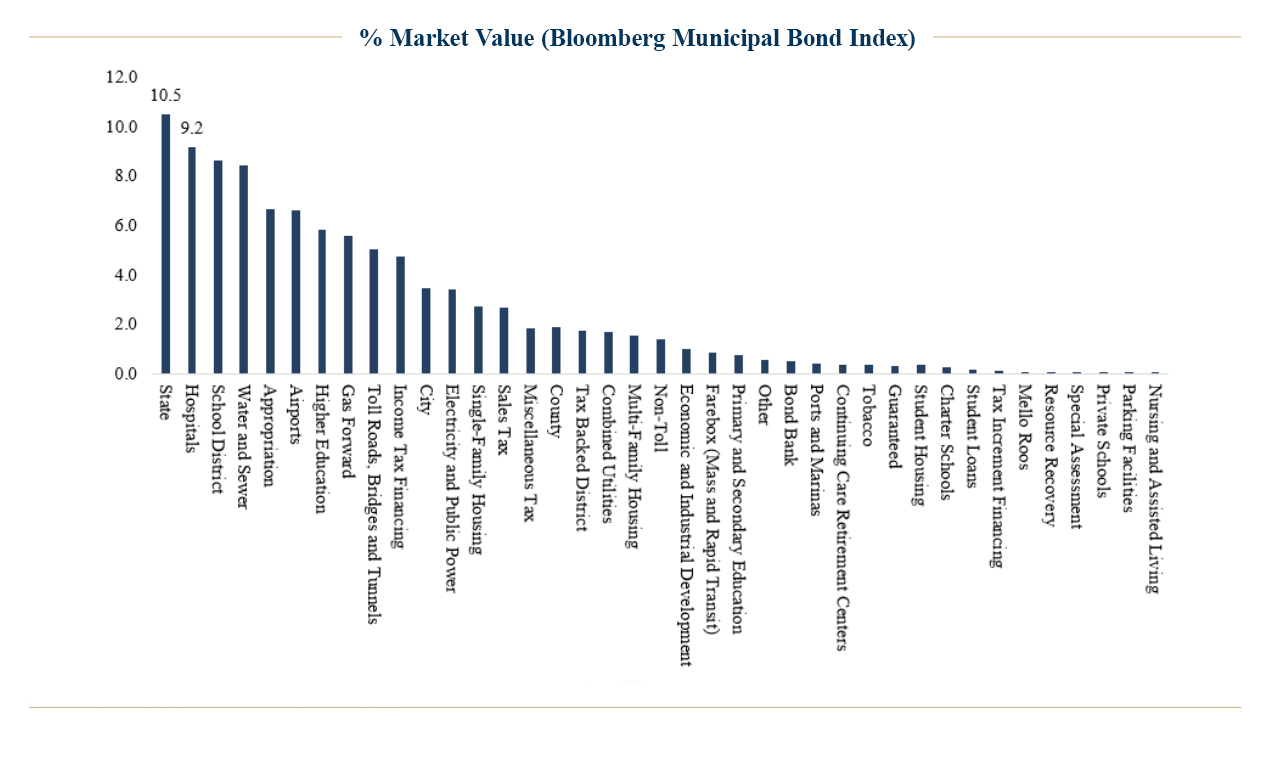

The hospital sector is one place where that distinction matters. Healthcare is a major component of the municipal market, and hospital bonds account for roughly 9.2% of the Bloomberg Municipal Bond Index market value, according to the data reviewed for this paper.i That alone makes the sector too large for document-level optionality to be treated as a legal footnote.

The issue is not whether religious-affiliated healthcare systems are good credit risks. Many are important institutions with significant scale, operating history, and market relevance. The issue is whether certain bond documents grant the issuer the right to redeem bonds at par under circumstances that may not be reflected in the yield an investor accepts at the time of purchase.

For investors who purchase premium municipal bonds, that distinction can be material.

The Size of the Reviewable Universe

Using the Bloomberg Municipal Bond Index as a proxy, the municipal market represented in the index included roughly $2.0 trillion as of June 9, 2026, compared with approximately $4.4 trillion of total municipal bonds outstanding, according to recent SIFMA statistics.ii Within the index, hospitals accounted for roughly 9.2% of market value, making healthcare one of the largest sectors, slightly behind states at 10.5%.iii

According to KFF, there are 6,093 hospitals in the United States. Of those, 5,112 are community hospitals, and 58% are nonprofit.iv Many nonprofit hospitals access the tax-exempt municipal market to finance capital projects, facilities, and system needs.

Religious affiliation is also a significant part of the healthcare landscape. Nearly 20% of hospitals in the United States have a religious affiliation, and the 10 largest Catholic healthcare systems collectively own about 50% of all short-term acute care hospitals.v

If one applies an illustrative 20% religious-affiliation screen to the hospital component of the Bloomberg Municipal Bond Index, the result is approximately $37 billion in bonds that may warrant targeted covenant review. This is a prioritization estimate. It is not a measured, callable universe, and it does not imply that every religious-affiliated hospital bond contains the same language or presents the same risk.

To us, it means the issue is significant enough to warrant systematic analysis.

| Factor | Value | Comment |

|---|---|---|

| Bloomberg Municipal Bond Index proxy | ~$2.0T | Investable benchmark proxy used for this analysis |

| Hospital sector share of index | 9.20% | Bloomberg sector data referenced in source materials, as of 06.09.26 |

| Implied hospital index exposure | ~$184B | 9.2% x ~$2.0T |

| Illustrative religious-affiliation screen | 20% | Approximation based on religious-affiliation estimates for U.S. hospitals |

| Exposure warranting document review | ~$37B | 20% x ~$184B; not a measured par-call universe |

The Provision That We Believe Should Get More Attention

The following language is from an actual bond document:

Extraordinary Optional Redemption. The Bonds are subject to extraordinary optional redemption prior to their Maturity Date, at the option of the Corporation, in whole or in part on any Business Day in such amounts as are designated by the Corporation, at a Redemption Price equal to the principal amount thereof plus interest accrued thereon, if any, to the date fixed for redemption, without premium … if (A) the Corporation or any other Member of the Obligated Group shall be legally required by reason of its being party to the Master Indenture, the Loan Agreement or any other document in connection with the issuance of the Bonds to perform any medical or surgical procedure, or otherwise to operate any of its health facilities in a manner, which the Corporation shall, in good faith, believe to be contrary to the principles of the General Conference of the Seventh-day Adventists (or any successor thereto) or (B) the Corporation shall believe in good faith that there is a substantial threat of the Corporation or any other Member being so required.vi

In plain English, this provision may allow the related healthcare system to redeem the bonds at par if it believes, in good faith, that it is legally required, or faces a substantial threat of being legally required, to perform a medical procedure or operate in a manner contrary to specified religious principles.

Extraordinary optional redemption provisions are not inherently unusual. Municipal bond documents often include special redemption rights tied to casualty, condemnation, tax events, or other defined circumstances. The distinctive feature here is the mission-conflict trigger. The borrower may have the right to redeem bonds at par if a legal requirement or a perceived substantial threat conflicts with stated religious principles.

For an investor, the key question is simple: Am I being paid enough for that issuer-side optionality?

Why We Believe Premium Buyers Should Care

Many municipal bonds are issued and traded at premiums. A premium municipal bond is bought above par, typically because its stated coupon exceeds prevailing market rates. That can be appropriate, and premium bonds are common in separately managed municipal portfolios.

The risk changes when a bond purchased above par can be unexpectedly redeemed at par.

Assume an investor pays 106.95 for a bond with a par value of 100. If the bond is redeemed at 100 earlier than expected, the investor receives less than the purchase price and may lose unamortized premium.vii The issue is not only that expected cash flows end sooner. It is possible that the investor may have accepted a yield that did not adequately account for a provision buried in the document.

In the example reviewed, the bonds were sold at 106.95.viii If a par redemption were triggered, the investor would not receive a make-whole payment or a call premium. The redemption price would be principal plus accrued interest, without premium. That is the asymmetry.

Credit quality may remain sound. The issuer may have no current intention to exercise the provision, and the trigger may never occur. Even so, we believe a prudent investor should not confuse low probability with irrelevance. A bond bought above par that includes an unusual par redemption right has a different risk profile than the same bond without that language.

The Market Should Treat Optionality as Credit Research

Municipal credit analysis has traditionally emphasized ratings, coverage, liquidity, debt service, management, market position, payer mix, and sector trends. Those remain essential, but the analysis is incomplete, we believe, if the investment process does not account for document-level optionality.

This matters because the municipal market is not uniform. Two bonds from similar issuers in the same sector, with similar ratings and maturities, can deliver materially different economic outcomes due to differences in redemption language. A portfolio that appears diversified by sector and issuer may still have concentrated exposure to unpriced optionality.

For UHNW investors, that matters. Municipal portfolios are often built for after-tax income, capital preservation, and controlled volatility. They are also often customized, held in separately managed accounts, and purchased in odd-lot or relationship-driven contexts, where document review can vary. In that environment, small differences in language can have significant consequences for realized return.

We believe, the appropriate response is not to avoid religious-affiliated healthcare bonds. That would be too blunt. Instead, the appropriate response is to identify the provision, understand the par-call scenario, assess the trigger language, evaluate price sensitivity, and incorporate the result into the investment decision.

In practice, that means asking several questions before purchasing. Does the bond include an extraordinary optional redemption provision tied to religious principles, mission conflict, medical procedures, legal requirements, or perceived threats? Is the redemption price at or above par? How much premium is embedded in the purchase price? What is the yield impact under an early redemption at par? Is the investor receiving adequate compensation for the risk?

If the answer to the last question is unclear, the bond needs more work.

The Larger Point

The municipal market is essential, efficient, and at times absurd. It finances hospitals, schools, roads, utilities, and public infrastructure. It also contains documents that can quietly allocate value between the issuer and the investor. That is not a market defect. It is a reason to read and research carefully.

Religion-affiliated healthcare bonds are a useful case study because they illustrate how legal language, public policy, healthcare operations, and investor economics can intersect within a single redemption provision. That provision may never be used, yet it may also determine whether a premium bond performs as expected.

For investors, the lesson is not theological but analytical. When buying premium municipal bonds, we believe the question cannot stop at whether the issuer is money good. The question is whether the structure is investor friendly.

ii SIFMA US Municipal Bond Statistics as of 06.02.26 https://www.sifma.org/research/statistics/us-municipal-bonds-statistics

iii Bloomberg Municipal Bond Index as of 06.09.26

iv https://www.kff.org/health-costs/key-facts-about-hospitals/

v Sage Journals Religious Hospitals and Poorer Health Outcomes: A Case Study Using Hospital Performance Ratings (06.24.25)

vi Adventist Health System/West Series 2024A Revenue Bonds

vii MSRB About Premium Municipal Bonds 2018.1

viii Bloomberg security description page, dated 05.23.24

Disclosure

A&M Private Wealth Partners, LLC (“AMPWP”) is an SEC-registered investment adviser. SEC registration does not imply a certain level of skill or training. For additional information on the services AMPWP provides, as well as our fees for such services, please review our Form ADV at adviserinfo.sec.gov, contact us at 300 Banyan Boulevard, 10th Floor, West Palm Beach, FL 33401, or call us at (561) 268-0900.

This piece and its content reflect AMPWP’s views at the time of its writing, and the information presented and AMPWP’s views are for informational purposes only. Such views are subject to change at any time without notice including due to changes in market or economic conditions, and forward-looking statements or forecasts are based on assumptions and may not be realized. Future events and outcomes are inherently uncertain. Statements are subject to risks and uncertainties that could cause actual outcomes to differ. AMPWP has obtained information provided herein from various third-party sources believed to be reliable, however, such information is not guaranteed and is subject to errors, omissions, and changes. No reliance should be placed on the views and information presented when making any investment or liquidation decision. AMPWP is not responsible for the consequences of any decisions or actions taken or not taken as a result of the views and information presented, and AMPWP does not warrant or guarantee the accuracy or completeness of this piece or information presented.

Additional content may be relevant for further context or other insight. Portfolios should also be viewed in the context of the broad market and general economic conditions prevailing during the periods covered by performance and other information. Any references to future returns and/or risk are not promises of the actual return a portfolio may achieve nor do they reflect all risks. Not all investments are suitable for all investors. All investments involve risk of loss, including to principal, and all investors must be prepared to bear such loss. Different securities, strategies, and allocations have different costs and risks, and diversification also does not assure a profit nor protect against a loss. Past performance is not a guarantee of future results. Additionally, changes in investment strategies, contributions, or withdrawals may materially alter results, as may market conditions, other factors including but limited to economic factors, fees, expenses, and events. Nothing herein should be construed as an investment recommendation. AMPWP does not provide legal, accounting, or tax advice, and AMPWP’s services are not intended to act as a substitute for such advice. AMPWP encourages you to seek the counsel of a qualified attorney and/or accountant for legal, accounting, or tax advice.